Retail Media Picked the World Cup to End the Argument. Incrementality Doesn't Take Sides.

Retail media has made the 2026 World Cup its public proving ground, betting that match-moment shopping ads will finally demonstrate the incrementality advertisers have doubted since 2024. But incrementality is a neutral test, and run honestly at this scale it can confirm the doubt as readily as dispel it.

Sir John Crabstone

Retail media has booked the World Cup as its proving ground. Walmart Connect and the grocery networks are selling shoppable spots and match-moment offers; Amazon Ads and Instacart have joined the field. Criteo’s retail-media president has pronounced the channel “no longer just a lower-funnel performance channel.” The spots are the visible part; the wager underneath is credibility. The sector has entered an examination, and the examiner is the one number it has spent two years failing to deliver: incrementality.

The scale of the wager is not in question. The tournament will push an extra $10.5 billion into global ad spend this quarter, per WARC Media, and retail media has cast itself as the chief beneficiary. It is the medium that converts a goal into a jersey sale before the replay ends; no other channel can match that speed. Every network wants the credit. Credit, in this business, is the product.

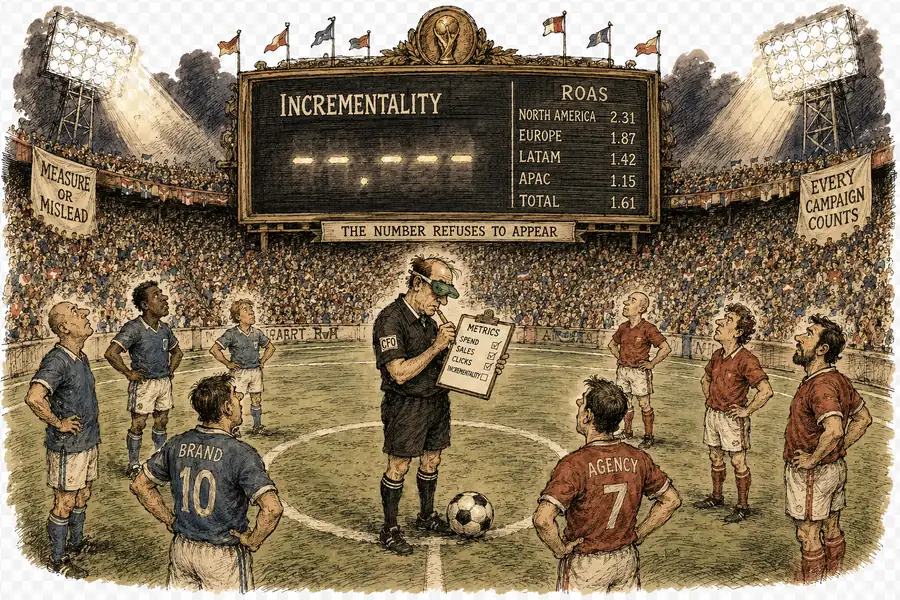

Advertisers are asking a colder question than who wins the broadcast. They want to know whether the ads sold them anything they would not have sold anyway. Skai, which sells retail media measurement software, partnered with Stratably to survey 166 retail-media advertisers spanning CPGs, agencies, and brands of every size: three in four named incrementality their hardest measurement problem, and just fifteen percent rated themselves highly effective at measuring the channel. The survey is self-commissioned; Skai’s platform is sold as the solution to the problem it describes. These are the buyers the World Cup is meant to convince, and they have registered their doubt plainly.

Incrementality has a plain definition and an uncomfortable result. Hold the ad back from a matched group of shoppers, compare what each group buys, and the difference is what the advertising caused. Run that test and the number is not a flattering measure — it is an honest one, almost always smaller than the last-click total the networks report. The gap between the two figures is the thing retail media has not been eager to discuss. The sector has long known how to run it. It has seldom offered to run it in the open; that is a choice, not an incapacity.

The World Cup is the hardest possible place to run it cleanly. 104 matches across a month, every day a final, budgets rewritten day by day: the baseline a holdout needs to mean anything keeps moving. Consumer demand shifts by match, by result, by the half-hour following a goal. A lift study that survives this noise would prove something real. Fail, and it will have measured the doubt instead of dispelling it.

One does not take a winning argument to the World Cup.

The tournament runs through 19 July; the reckoning does not. A lift study returns whatever it returns, on its own schedule, weeks after the trophy is lifted. The advertisers will receive those numbers before the networks are ready to frame them. Retail media spent two years deferring this number. It chose the loudest room in the world to read it aloud.