America Closed De Minimis. Ozon Counted The Sellers.

Ozon compounded GMV at 91% a year between 2017 and 2025 while Washington and Brussels closed the parcel lanes Chinese sellers had used to reach Western consumers. The two trends describe one re-routed trade, and the Russian platform is the toll booth.

Neritus Vale

Ozon compounded gross merchandise value at 91% a year between 2017 and 2025, by its own account. In the same year the curve closed out, Washington and Brussels both shut the parcel lanes Chinese sellers had used to reach US and EU consumers without paying full duty. These are not two stories. They are one re-routed trade, and Ozon is the toll booth.

The pitch is structural under-penetration. Russia’s e-commerce share of retail sits at roughly 23%, late by Chinese standards but climbing; the president of Ozon Greater China, Simon Huang, told 36Kr the platform now hosts over 750,000 active sellers. Headroom of that size is what lets the platform publish growth numbers Western analysts last saw at Alibaba’s IPO. Russian retail spent the last three years losing Western brands and gaining Chinese substitutes. Ozon did not invent the demand; it built the rails that let Yiwu meet Yekaterinburg.

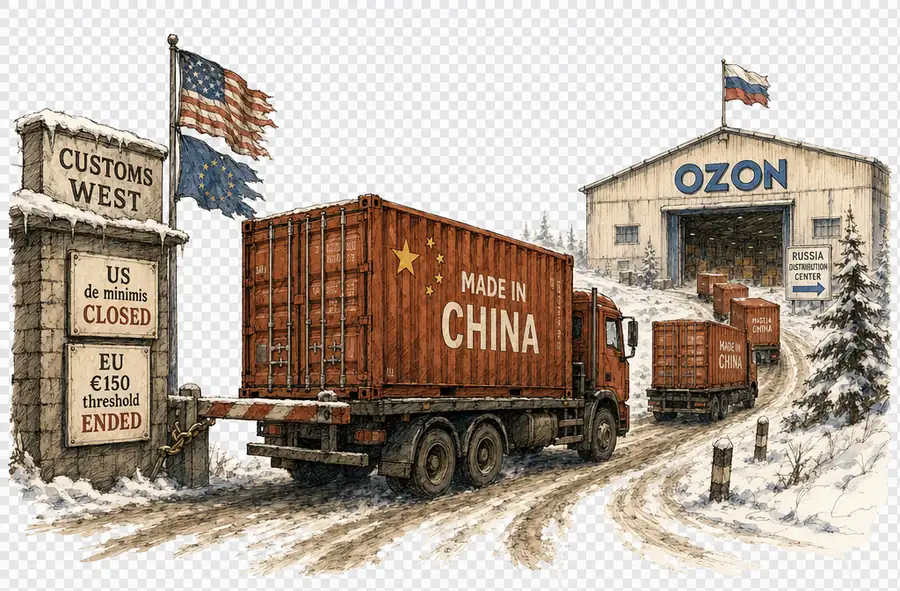

The lane through Russia matters now because the lanes through the West have narrowed. The US ended its $800 de minimis exemption for shipments from China and Hong Kong in 2025. That threshold had served as the structural subsidy beneath Temu’s and Shein’s American pricing. The EU’s finance ministers scrapped the parallel €150 threshold in December 2025, with implementation rolling through 2026. What disappeared was the business model the regulation had been quietly subsidising.

By late 2022, with Western brands clearing Russian shelves, Chinese-origin goods had reached 90% of Ozon’s cross-border trade, as TechNode reported from the South China Morning Post, and the platform opened a Shenzhen office to recruit more merchants. That concentration was exit-driven; what followed is structural. Chinese merchants now account for more than a fifth of Ozon’s seller base, and the platform announced plans to open six new distribution centres in Hangzhou, Dongguan, Yiwu, Shanghai, Alashankou, and Dongning. The infrastructure is the message: Ozon built lanes for the sellers Washington and Brussels were preparing to evict.

The logistics density does the rest of the work. Ozon has built more than 5 million square metres of warehousing, and the inventory cycling through it is increasingly Chinese. The self-pickup network covers 90% of Russian users, which is the kind of address-book number that does not show up in a price comparison. That density is not retrievable through a price cut. A Chinese seller migrating to Ozon Global inherits a cost structure that prices Russian distance as Ozon’s problem rather than theirs. The Western brand exit gave Chinese sellers a buyer; the warehouses gave them a contract that survives whichever way the politics turn next.

Russia is not a substitute for America, and the sellers who confuse the two will discover the difference at the next currency print.

The counter-argument deserves its best form, which is that Ozon’s compound rate is a function of Russia being sanctioned rather than of Russia being a real market. The ruble is volatile, capital controls block repatriation, and Western brand exits — not consumer wealth — gave Chinese sellers their lane. If the war ends, Western retailers return, and sanctions ease, that compound rate becomes the artefact of a closed window rather than the curve of a new one. The argument is serious. It is also incomplete.

It is incomplete because the under-penetration would not disappear in a thaw. Structural under-penetration leaves Ozon with the warehouses, the pickup network, and the seller relationships regardless of which brands return to Moscow shelves. Ozon raised its 2025 guidance to roughly 40% GMV growth, against a base already inflated by 2024’s run; the platform recorded a 7.9 billion ruble net loss in Q1 2025 and expected none for the year. The growth has stopped being brand-substitution and become buyer habit. The geopolitical risk is real, and so is the platform moat the geopolitics created.

What Chinese sellers are choosing is exposure to ruble cash flows in exchange for a lane that prices at margin rather than at tariff. That is a trade with a price. The price of admission is currency risk, sanctions secondary-exposure risk, and a deepening commercial dependency on a regime that Washington and Brussels are still trying to isolate. Ozon will keep compounding. Whether the rouble compounds with it is a question the platform does not answer. And whether either survives a settlement neither party controls is the only number worth tracking.