Alibaba Pledged ¥380 Billion. Three Rivals Already Took The Ground.

Alibaba's ¥380 billion AI infrastructure pledge is defensive capex, buying back commerce ground Pinduoduo's pricing, JD's hiring, and Douyin's shelf traffic have already taken at a fraction of the cost.

Sir John Crabstone

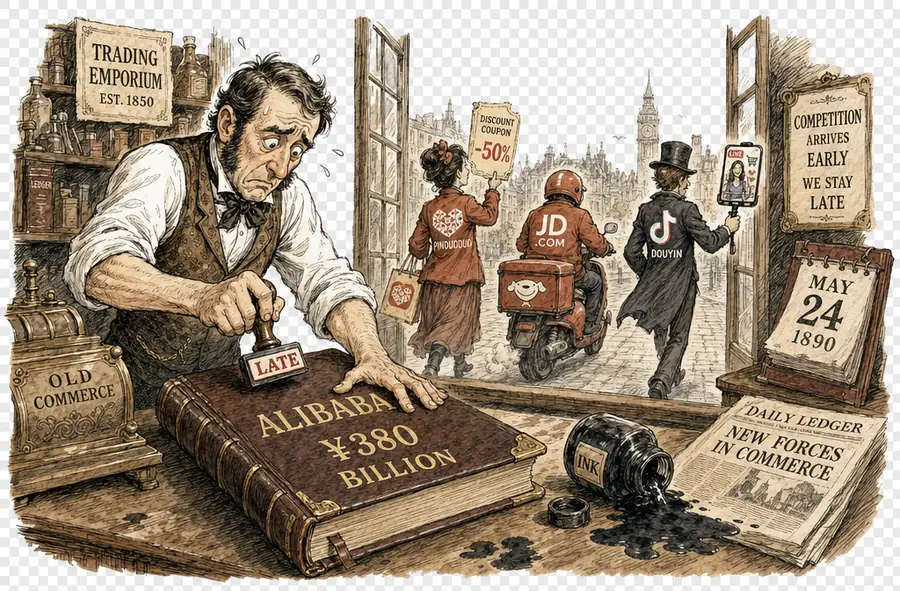

Eddie Wu calls his ¥380 billion AI capex pledge “on the small side.” In the courteous vocabulary of Chinese tech, that is what surrender sounds like to a shareholder. The cheque Wu announced in February 2025 exceeds Alibaba’s total AI and cloud spending over the past decade, and he has hinted it will rise. The number is impressive; the rationale is not. It does not buy Alibaba a future it could not otherwise reach. It buys back a present three rivals already took with cheaper instruments.

Pinduoduo did not need a fab to win on price. Its model runs on warehouse discipline rather than transformer count; it competed on cost, and cost cannot be AI-generated. The gap it cut in the years Alibaba was ordering chips has not closed. You cannot caffeinate a coupon with a large language model; you can only pay for the coupon.

JD has been more candid about the means. It committed to fifty thousand delivery hires as a first step into the fast-delivery market Meituan owns. Train shoppers to come for a meal and keep them for the toothpaste. The capability scales by paycheque, not by parameter; the bottleneck is HR, not silicon.

Douyin built the third front almost for free. ByteDance’s commerce business cleared roughly ¥3.5 trillion of GMV in 2024, as reported by 36Kr, with GMV now split roughly 4:3:3 among shelf sales, store livestreaming, and influencer livestreaming. Influencer-led live commerce, once the platform’s signature, now accounts for around 30% of total GMV. The compute was amortised by short-form video years ago; Douyin’s commerce is the resale. Alibaba’s ¥380 billion has no such shortcut — it must pay its way through the shop.

Alibaba Cloud’s AI revenue has grown in triple digits for nine consecutive quarters, which is the right answer to the wrong question. Cloud sells AI to other people’s businesses, not to Taobao’s shoppers. The capex must justify itself twice: once at the infrastructure layer, where Alibaba leads, and once at the commerce layer, where it is losing. The first is going well. The second is the reason for the ¥380 billion, and three rivals reached it years ago without the cheque.

The defensive shape of Alibaba’s own response is the most honest evidence. Taobao Instant Commerce launched in April; sales and marketing climbed to 21.5% of revenue from 13.4% a year earlier, and free cash flow turned negative by ¥18.8 billion. The capex pays for the silicon. Keeping the customers costs Alibaba another 8.1 points of revenue, burned on a Taobao that is no longer the cheapest, fastest, or most discoverable destination on the phone.

The position will be repurchased in silicon; whether the customers come back is a separate cheque.